🚀 July 11 Update – Batch Edit, Re-Quote, Tiered Pricing & Notifications Are Here

Dear Valued Customer,

We've just released another major update with improvements across the Instant Quote, Cart, Checkout, Dashboard, and Order Management.

As we're continuously shipping new features, there may still be occasional bugs or unexpected issues. If you find anything that doesn't work as expected, please let us know—we truly appreciate your feedback and will fix it as quickly as possible.

🛠 Instant Quote

🏷 Material Tags added to help you choose the most suitable material. 📊 Tiered Pricing is now available. Instantly compare quantity discounts and select the best pricing option. ✏️ Batch Edit for multiple parts. Update configurations or delete multiple parts at once.

🛒 Cart

🔄 Re-Quote any part directly from your cart and continue editing before placing your order. 🛍 Mini Cart added to the header, allowing you to quickly view your cart from any page.

📦 Orders

♻️ Add to Quote and Add All to Quote are now available for existing orders. Reuse previous parts, make changes, and generate a new quote in just one click.

💳 Checkout

🌍 Customs & Shipping Options added.

Choose how you want customs declaration handled. Set your preferred Customs Value. Tell us your Expected Shipping Date.

🔔 Dashboard

🔔 Notifications keep you updated on order status and important activities. 📢 Announcements provide the latest ProtoTi news and product updates.

⚡ Performance & Improvements

We've also fixed and optimized numerous issues across:

Instant Quote

Checkout

Order Details

making the overall experience smoother and more reliable.

💬 Found a bug or have a feature request?

We're releasing new features rapidly, and your feedback helps us improve faster.

VoxelMatters published its first vertical market study on AM of Lifestyle, Design and Luxury Products, forecasting a business that will top $28 billion yearly by 2033

🌟Content in this article

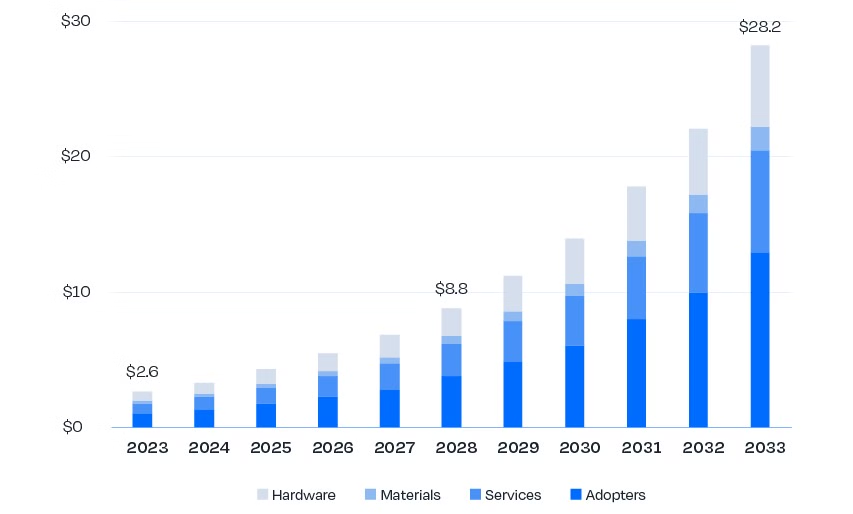

The AM market for Consumer Products, valued at $2.6 billion in 2023, is driven by end-user applications and is projected to grow significantly. VoxelMatters’ first vertical market study on Lifestyle, Design, and Luxury Products forecasts that the AM business will reach over $28 billion annually by 2033. This report underscores the growing importance of 3D printed consumer products in the additive manufacturing industry, highlighting their superior performance, efficiency, and customization.

The study covers several categories of commonly available 3D printed consumer products, including Lifestyle Products (such as Eyewear, Footwear, Sports Equipment and Consumer Electronics), Design Products (including furniture and high fashion items), and Luxury Products (like Jewelry and watchmaking). Segment-specific data is available throughout the report for hardware, material and parts demand and revenues.

A final-parts-driven AM market

The analysis of the current AM market for Consumer Products reveals a significant growth trajectory. In 2023, the overall value of AM products across all relevant consumer product segments reached $2.6 billion, up from $2.1 billion in 2022, marking a year-over-year growth of 24.7%. This figure includes all metal and polymer AM hardware and materials sold to various consumer product adoption verticals, and revenues from parts produced by AM service providers and internally by end-users across multiple adoption verticals.

The analysis indicates that while AM services remain the largest target segment for AM companies producing hardware and materials for consumer products manufacturing, the combined value of parts produced internally by end-users represents an even larger opportunity. Internal production of parts, including prototypes, tools, and final parts, accounts for almost 39% of the total value generated, while parts produced externally by AM services represent another 29%.

This suggests that AM parts drive significant investments in AM for consumer products, totaling nearly $1.8 billion in 2023. Notably, $188 million worth of materials (polymer and metals) was sold in 2023 to produce these parts, indicating that final 3D printed parts are valued at approximately ten times the material cost, which fuels investments in hardware. Polymers dominate the business, being over four times larger than metals, due to the current limitations of metal AM technologies in meeting high productivity demands.

Huge and realistic future opportunities

The overall revenue for AM in the consumer products market is projected to grow from $2.6 billion in 2023 to $28.2 billion in 2033, achieving a compound annual growth rate (CAGR) of 26.8%. This significant assessment covers the entire value chain of AM across all consumer product segments, including AM hardware, materials, and parts produced by both AM services and (internally) by vertical end-users. Despite this substantial growth, the projected $28.2 billion in revenue represents only a small fraction of the overall consumer products market, which generates trillions of dollars annually. This conservative and accurate forecast highlights that while consumer products are a major vertical for AM, the AM industry as a whole is on track to reach $100 to $200 billion in revenue by the mid-2030s.

VoxelMatters Research’s first vertical market study focuses on consumer products, combining specific data and information from their previous Core AM market studies with new data from known end-users of additive manufacturing. The study covers three key verticals—Lifestyle Products, Design Products, and Luxury Products—and eight sub-verticals, including Footwear, Eyewear, Sports Equipment, Consumer Electronics, Toys, Fashion, along with Design Products and Luxury Products. The data collection methodology leverages extensive data from VoxelMatters’ Core AM reports on Polymer AM and Metal AM, including niche areas like Ceramic AM. This report is based on data from 1,346 core AM operators, representing nearly 1,241 unique companies, including end-users, all listed in the VoxelMatters Directory.

Key data and insights were collected through an extensive survey from stakeholders and compared with publicly available information on revenue and production capabilities for each company. VoxelMatters Research also conducted interviews with AM and consumer products industry operators and independent consultants to verify the collected data, estimates, and analyses. Prominent and emerging core AM companies featured in the report include 3D Systems, Airtech, Anycubic, ARRIS, BASF Forward AM, Bambu Lab, Caracol, Carbon, Cooksongold, Creality, Digital Metal (Markforged), EOS, Evonik, ExOne, ETEC (Desktop Metal), Formlabs, Genera, Greenfill3D, HP 3D Printing, Legor, Luxcreo, Materialise, Massivit, MX3D, OECHSLER, Progol3D, Prusa Research, Raise3D, Shapeways, Stratasys, Ultimaker, voxeljet, and others. End-user companies surveyed and analyzed include adidas, Aectual, Apple, Barrelhand, Beretta, Brooks Running, COBRA, Dior, Elli Design, Götti, Grohe, Hoet, Honor, Hoya, King Children, Kohler, LEGO, Luxottica, Meta, Microsoft, Mikita, MONOQOOL, New Balance, Nike, nVidia, PEAK, Pinarello, Posedla, Puma, Riddel, Safilo, Scope, Sennheiser, Signify (Philips), Specialized, Superfeet, The New Raw, Wilson, YOU MAWO, Zellerfeld, and many others.